How to Pay Yourself From a Corporation in Canada: Salary, Dividends, or Both?

Running a corporation in Canada brings many advantages—tax flexibility, liability protection, and the ability to control how you take income from your business. Yet one of the first questions every incorporated entrepreneur eventually asks is simple but surprisingly complex: How should I pay myself?

Unlike sole proprietors who simply withdraw money from their business profits, incorporated business owners have structured options. The two primary methods are salary and dividends, and in many situations a mix of both. The decision you make can affect your taxes, retirement planning, cash flow, and even your ability to get a mortgage.

Canadian tax rules allow owners to choose the compensation strategy that fits their financial goals. However, the difference between these options is not just technical—it can mean saving or losing thousands of dollars in taxes each year. Many new business owners default to one option without realizing how much flexibility they actually have.

Think of it like choosing how to fuel a car. Salary is like gasoline: reliable, predictable, and structured. Dividends are more like electric power: efficient in certain situations but dependent on your overall system. When used together, they can create the most efficient financial engine.

This guide explains how salary, dividends, and mixed strategies work in Canada, how taxes apply to each method, and how small business owners can choose the most tax-efficient way to pay themselves.

Understanding Owner Compensation in a Canadian Corporation

Why Paying Yourself Correctly Matters

Paying yourself from your corporation is more than simply transferring money from a business bank account to your personal account. The way you structure this payment determines how taxes are applied, how your corporation reports income, and how government programs like retirement benefits treat your earnings.

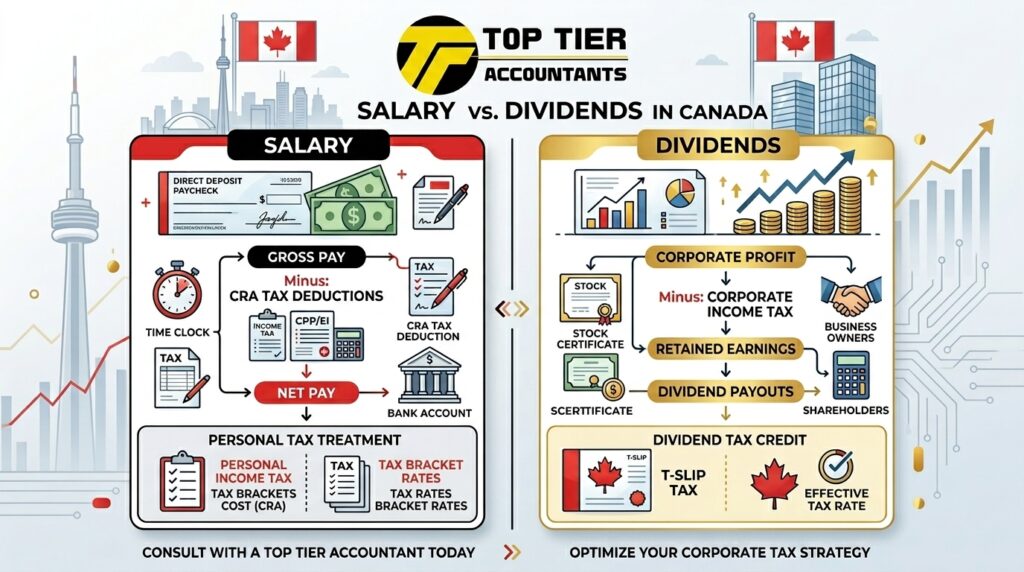

A corporation is legally separate from its owner. Because of this separation, you cannot simply withdraw money like you would from a personal account. Instead, payments must be classified as either salary (employment income) or dividends (shareholder income).

Each option creates different tax consequences. For example, salaries are considered business expenses, which means they reduce the corporation’s taxable income. Dividends, on the other hand, are paid from profits after corporate tax has already been applied.

The Canadian tax system attempts to maintain something called tax integration, meaning the total tax paid should be roughly similar whether income is earned through a corporation or personally. In theory, this prevents people from avoiding taxes simply by incorporating. In reality, the system is not perfectly balanced, and small differences can create opportunities for Strategic Tax Planning.

Business owners must also consider long-term implications. Salary contributes to retirement programs such as the Canada Pension Plan and creates RRSP contribution room. Dividends do not. These details may not seem important during the early years of a business, but over time they can dramatically influence retirement savings and financial security.

Choosing the right compensation method is therefore less about finding a universal rule and more about aligning your pay structure with your long-term goals.

The Two Main Ways to Pay Yourself

In Canada, incorporated business owners generally have two ways to take money from their company:

- Salary

- Dividends

Both methods are legal and widely used, but they function very differently from an accounting and tax perspective.

A salary is treated as employment income. When a corporation pays a salary to its owner, it must run payroll just like any other employer. This includes withholding income tax and making Canada Pension Plan (CPP) contributions before remitting them to the government.

A dividend, by contrast, is a distribution of profits to shareholders. Instead of payroll deductions, dividends are declared by the corporation and paid out of retained earnings after corporate tax has already been paid.

The choice between these options is rarely straightforward. Some business owners prefer the predictability of a regular salary, while others appreciate the simplicity and tax advantages of dividends. Many experienced entrepreneurs ultimately combine the two to create a balanced compensation strategy.

Understanding how each method works is the first step toward designing the most tax-efficient approach for your corporation.

Paying Yourself a Salary From Your Corporation

How Salary Works in a Corporation

When you pay yourself a salary from your corporation, you are essentially acting as both employee and employer. The corporation issues you a paycheck, deducts payroll taxes, and reports your earnings through a T4 slip at the end of the year.

This process is similar to how traditional employees are paid. The corporation must deduct income tax and Canada Pension Plan contributions from each paycheck and remit them to the government.

From the corporation’s perspective, salary is considered an operating expense. This means the payment reduces the company’s taxable income. For example, if your corporation earns $150,000 in profit and pays you a $70,000 salary, the company is taxed only on the remaining profit.

Because salary reduces corporate income, it can be a useful tool for controlling how much tax the corporation pays. Many business owners use salaries to keep their corporate income within the small business tax rate threshold.

Another important aspect of salary is timing. Salaries can be paid regularly throughout the year—weekly, biweekly, or monthly—creating predictable personal income. This consistency can be especially valuable for budgeting, personal expenses, and qualifying for loans or mortgages.

For many entrepreneurs, salary provides structure and stability that dividends alone cannot offer.

Advantages of Paying Yourself a Salary

Choosing salary as your primary form of compensation offers several advantages, particularly for business owners who value stability and long-term financial planning.

First, salary creates RRSP contribution room. In Canada, RRSP limits are based on earned income, and salary qualifies as earned income. Dividends do not. Over time, this difference can significantly affect how much tax-deferred retirement savings you can accumulate.

Second, salary contributes to the Canada Pension Plan. These contributions build retirement benefits that provide income later in life. For entrepreneurs who want guaranteed retirement income, this can be a valuable benefit.

Another advantage is financial credibility. Lenders and mortgage providers often prefer applicants with stable employment income. A consistent salary can make it easier to qualify for mortgages, loans, or credit lines.

Salary also simplifies personal tax planning because taxes are deducted at the source. This reduces the risk of large unexpected tax bills at the end of the year.

For business owners seeking predictable income, structured retirement planning, and easier access to financing, salary can be a powerful tool.

Disadvantages of Salary

Despite its advantages, salary also has drawbacks that business owners must consider.

The biggest downside is payroll tax obligations. Both the employee and employer portions of CPP contributions must be paid when salary is issued. This effectively doubles the CPP cost compared to traditional employees.

Salary also requires more administrative work. Running payroll involves calculating deductions, remitting taxes, and filing payroll reports with the government. For small corporations without accounting software or professional support, this process can feel cumbersome.

Another limitation is flexibility. Once payroll schedules are established, adjusting salary payments can require additional paperwork and compliance steps.

Some business owners also find salary less tax-efficient at higher income levels compared to dividends, depending on provincial tax rates.

These factors often lead entrepreneurs to explore dividend payments as an alternative or supplement.

Paying Yourself Dividends

How Dividends Work in Canada

Dividends represent profits distributed to shareholders after the corporation has paid corporate tax. Instead of receiving a paycheck, you receive a dividend payment based on the company’s retained earnings.

When dividends are issued, the corporation provides shareholders with a T5 slip reporting the amount received. Unlike salary, no payroll deductions are taken from the payment.

Dividends are taxed differently because Canada uses a system called the dividend gross-up and tax credit, which is designed to prevent double taxation.

Under this system, dividends are first “grossed up” to reflect the corporation’s pre-tax income. Then a dividend tax credit reduces the personal tax owed. This mechanism ensures that corporate income is not unfairly taxed twice.

Because of these tax credits, dividends often result in lower personal tax rates compared with salary, depending on income level and province.

For business owners seeking simplicity and tax efficiency, dividends can be an attractive option.

Advantages of Dividends

Dividends offer several benefits that make them appealing to many entrepreneurs.

One major advantage is simplicity. Dividends do not require payroll deductions or ongoing remittances. Instead, they can be declared periodically and paid directly to shareholders.

Another advantage is no CPP contributions. Since dividends are not considered employment income, they are not subject to Canada Pension Plan premiums. This can result in immediate cash savings.

Dividends may also produce lower personal tax rates because of the dividend tax credit system. In some provinces, certain dividend income can be taxed at rates significantly lower than equivalent salary income.

These benefits make dividends particularly attractive for business owners who prefer flexibility and reduced payroll complexity.

Disadvantages of Dividends

Despite their advantages, dividends also have several important limitations.

First, dividends do not generate RRSP contribution room, which can limit retirement savings opportunities. For business owners relying heavily on dividends, this can reduce tax-advantaged investment options.

Second, dividends do not contribute to CPP retirement benefits. While avoiding CPP contributions may increase short-term income, it can also reduce guaranteed retirement income later in life.

Dividends can also create cash flow challenges because personal taxes are not withheld at the time of payment. Business owners must set aside funds to cover personal tax obligations when filing their returns.

Finally, dividends must come from after-tax corporate profits, meaning the corporation has already paid corporate tax before distributing the income.

These limitations highlight why many entrepreneurs eventually adopt a blended approach.

Salary vs Dividends – Key Tax Differences

Corporate Tax Impact

From the corporation’s perspective, the tax treatment of salary and dividends is dramatically different.

Salary is considered a deductible expense. When a corporation pays salary to its owner, the payment reduces taxable income and therefore lowers corporate tax.

Dividends, by contrast, are paid from profits after corporate taxes have already been calculated. This means dividends do not reduce corporate taxable income.

For corporations earning large profits, salaries can help manage corporate tax exposure. By paying a portion of profits as salary, owners can control how much income remains within the corporation.

Personal Tax Impact

At the personal level, the tax treatment also differs significantly.

Salary is taxed as employment income, subject to regular federal and provincial income tax rates. Canada uses progressive tax brackets, meaning higher income levels face higher tax rates.

Dividends are taxed through the gross-up and dividend tax credit system, which can lower effective tax rates compared to salary income.

The actual difference depends heavily on province, income level, and other deductions. In many situations, the total combined tax (corporate plus personal) is similar between the two methods due to Canada’s integration system.

However, small variations can still create meaningful tax savings depending on individual circumstances.

Using a Combination Strategy

Why Many Business Owners Choose Both

Experienced accountants often recommend a hybrid approach that combines salary and dividends. This strategy allows business owners to capture the advantages of both methods while minimizing their drawbacks.

For example, salary can be used to generate RRSP contribution room and maintain CPP participation, while dividends can supplement income with potentially lower personal tax rates.

This approach also improves flexibility. During years when the corporation has strong profits, dividends can be increased. During slower periods, salary can remain stable to maintain predictable personal income.

The hybrid strategy is popular because it balances tax efficiency with long-term financial planning.

Example of a Salary + Dividend Strategy

Imagine a corporation earning $200,000 in profit before owner compensation.

A business owner might choose to:

- Pay $80,000 salary

- Take $70,000 dividends

- Leave the remaining income inside the corporation

The salary provides RRSP room and CPP benefits, while dividends reduce payroll taxes and increase net income.

The remaining profits can stay inside the corporation for reinvestment or future dividends.

This balanced strategy often delivers both tax efficiency and financial stability.

Factors That Determine the Best Option

Your Income Level

Your personal income bracket plays a major role in determining the best compensation strategy.

Higher-income individuals may benefit from dividends due to preferential tax treatment. Lower-income individuals may see minimal differences between salary and dividends.

Retirement Planning (CPP and RRSP)

If building retirement savings is a priority, salary becomes more attractive because it generates RRSP contribution room and CPP benefits.

Dividends may increase current income but do not support these retirement programs.

Business Cash Flow

Cash flow also influences compensation decisions.

Startups may rely on dividends because they are flexible and require less administrative overhead. Mature businesses with steady income may prefer structured salaries.

Common Mistakes When Paying Yourself

Many new business owners make costly mistakes when deciding how to pay themselves.

Some rely exclusively on dividends without considering retirement planning. Others pay large salaries without understanding payroll tax implications.

Another frequent mistake is failing to set aside funds for personal taxes when receiving dividends.

Working with an experienced accountant can help avoid these issues and create a customized compensation strategy.

Conclusion

Deciding how to pay yourself from a Canadian corporation is one of the most important financial choices you’ll make as a business owner. Salary, dividends, and hybrid strategies all offer different advantages depending on your financial goals, tax situation, and stage of Business Growth.

Salary provides structure, retirement benefits, and predictable income. Dividends offer simplicity and potential tax efficiency. Combining both often creates the most balanced strategy.

The best approach ultimately depends on factors such as income level, cash flow, and long-term planning. With careful strategy and professional guidance you can structure your compensation to maximize tax efficiency while building a strong financial future.

FAQs

1. Can I pay myself both salary and dividends in Canada?

Yes. Many business owners use a combination of salary and dividends to balance tax efficiency, retirement planning, and cash flow.

2. Do dividends require payroll deductions?

No. Dividends are paid from corporate profits and do not require payroll deductions like salary.

3. Does salary reduce corporate tax?

Yes. Salary is considered a business expense and reduces the corporation’s taxable income.

4. Do dividends count toward RRSP contribution room?

No. Only earned income, such as salary, creates RRSP contribution room.

5. What is the most tax-efficient way to pay yourself?

There is no universal answer. The most tax-efficient approach depends on your income, province, retirement goals, and business profitability.

Post a comment

Related Posts

June 5, 2026

What Expenses Are Tax Deductible for Small Businesses in Canada?

What Expenses Are Tax Deductible for Small Businesses in Canada? Running a small business in…

June 4, 2026

Small Business Tax Planning in Canada: Strategies to Reduce Your Tax Bill

Small Business Tax Planning in Canada: Strategies to Reduce Your Tax Bill Running a small…

June 4, 2026

Common Bookkeeping Mistakes Small Businesses Make in Canada

Common Bookkeeping Mistakes Small Businesses Make in Canada Running a small business in Canada is…

June 4, 2026

Cash vs Accrual Accounting in Canada: Which Method Is Better for Your Business?

Cash vs Accrual Accounting in Canada: Which Method Is Better for Your Business? Running a…