Small Business Tax Planning in Canada: Strategies to Reduce Your Tax Bill

Running a small business in Canada is exciting but let’s be honest, taxes can feel like navigating a maze. One wrong turn and suddenly thousands of dollars disappear from your profits. That’s why Tax Planning is one of the most powerful financial strategies any entrepreneur can implement. Instead of waiting until tax season to see what you owe, smart business owners plan throughout the year to reduce their tax bill legally.

Canada actually offers many opportunities for tax savings. With the right strategies, business owners can lower their tax burden through deductions, credits, business structure decisions, and income timing strategies. These tools are not loopholes—they are intentional policies designed to encourage entrepreneurship and business growth.

The numbers alone highlight how valuable tax planning can be. Canada has over 1.19 million small and medium-sized businesses, making them a major driver of the economy. Yet many owners still miss key deductions or planning opportunities that could save thousands annually.

If you’ve ever wondered how experienced entrepreneurs keep more of their profits, the answer usually isn’t luck. It’s proactive tax planning. Let’s explore the strategies that help Canadian small businesses legally reduce taxes while staying compliant.

Why Tax Planning Matters for Canadian Small Businesses

Tax planning is often misunderstood as something only large corporations need. In reality, small businesses benefit even more from effective tax strategies. When your margins are tight and every dollar counts, reducing taxes can significantly improve cash flow.

Many entrepreneurs focus entirely on generating revenue. They pour energy into marketing, hiring, and product development—but overlook the financial structure of their business. Without tax planning, a business might unknowingly pay thousands more in taxes than necessary.

Think of taxes like a leak in a water tank. You can keep pouring more water into the tank (revenue), but if the leak isn’t fixed (tax inefficiency), you’re constantly losing resources. Tax planning plugs those leaks.

Smart planning also helps businesses:

- Maintain healthier cash flow

- Reinvest profits into growth

- Avoid penalties and audits

- Plan future expansion strategically

This isn’t about avoiding taxes it’s about understanding how the system works and using it intelligently.

The Canadian Small Business Tax Landscape

Canada offers one of the most favorable tax systems for small incorporated businesses. Through the Small Business Deduction (SBD), eligible companies pay significantly lower corporate tax rates on their first portion of income.

The federal corporate tax rate for small businesses is 9% on the first $500,000 of active business income, compared to the general corporate rate of 15%.

When provincial taxes are included, the combined rate usually falls between 11% and 13% depending on the province.

Compare that to personal income tax rates that can exceed 50% in some provinces, and you can see why incorporation and strategic planning are so powerful.

Common Tax Mistakes That Cost Business Owners Money

Even experienced entrepreneurs make tax mistakes. The most common errors include:

- Mixing personal and business finances

- Missing eligible deductions

- Not planning salary vs dividend payments

- Poor receipt and expense tracking

- Waiting until tax season to think about taxes

Many small business owners claim only 50–70% of eligible deductions, leaving significant tax savings unclaimed each year.

Avoiding these mistakes is often the fastest way to reduce your tax bill.

Understanding the Small Business Tax Rate in Canada

To reduce taxes effectively, you must understand how business taxes work in Canada. Many entrepreneurs mistakenly focus only on deductions, but tax rates and structure decisions are equally important.

Federal Small Business Deduction Explained

The Small Business Deduction (SBD) is one of the most valuable tax advantages available to Canadian entrepreneurs.

It allows Canadian-Controlled Private Corporations (CCPCs) to pay a reduced federal tax rate of 9% on the first $500,000 of active business income.

Without this deduction, the general federal corporate rate would be 15%, meaning businesses could pay thousands more in taxes annually.

For example:

| Scenario | Corporate Tax Rate |

| Small business deduction | 9% |

| General corporate rate | 15% |

This difference alone can save up to $30,000 annually on qualifying income.

That’s money that can be reinvested into marketing, hiring, equipment, or expansion.

Provincial Tax Rates and Combined Corporate Taxes

In Canada, corporate taxes are split between federal and provincial governments. This means the total rate varies depending on where your business operates.

Here’s a simplified comparison:

| Province | Small Business Tax Rate | General Corporate Rate |

| Ontario | 12.2% | 26.5% |

| British Columbia | 11% | 27% |

| Alberta | 11% | 23% |

| Quebec | 12.2% | 26.5% |

The difference between small business and general corporate rates can exceed 14 percentage points, which makes tax planning extremely valuable.

Choosing the Right Business Structure

Your business structure has a major impact on how much tax you pay.

In Canada, businesses generally operate as:

- Sole proprietorships

- Partnerships

- Corporations

Each structure has different tax implications.

Sole Proprietorship vs Corporation

Sole proprietors report their business income on their personal tax return. This means profits are taxed at personal marginal tax rates, which can exceed 50% in some provinces.

Corporations, however, pay corporate tax rates first. This allows owners to leave money inside the company at lower tax rates, creating a tax deferral advantage.

This doesn’t mean incorporation is always the best option. For smaller businesses or side hustles, the administrative costs may outweigh the tax savings.

When Incorporation Reduces Taxes

Incorporation becomes beneficial when:

- Your business generates consistent profits

- You don’t need to withdraw all profits personally

- You want liability protection

- You plan to scale the business

The ability to retain earnings at lower tax rates allows businesses to reinvest profits and grow faster.

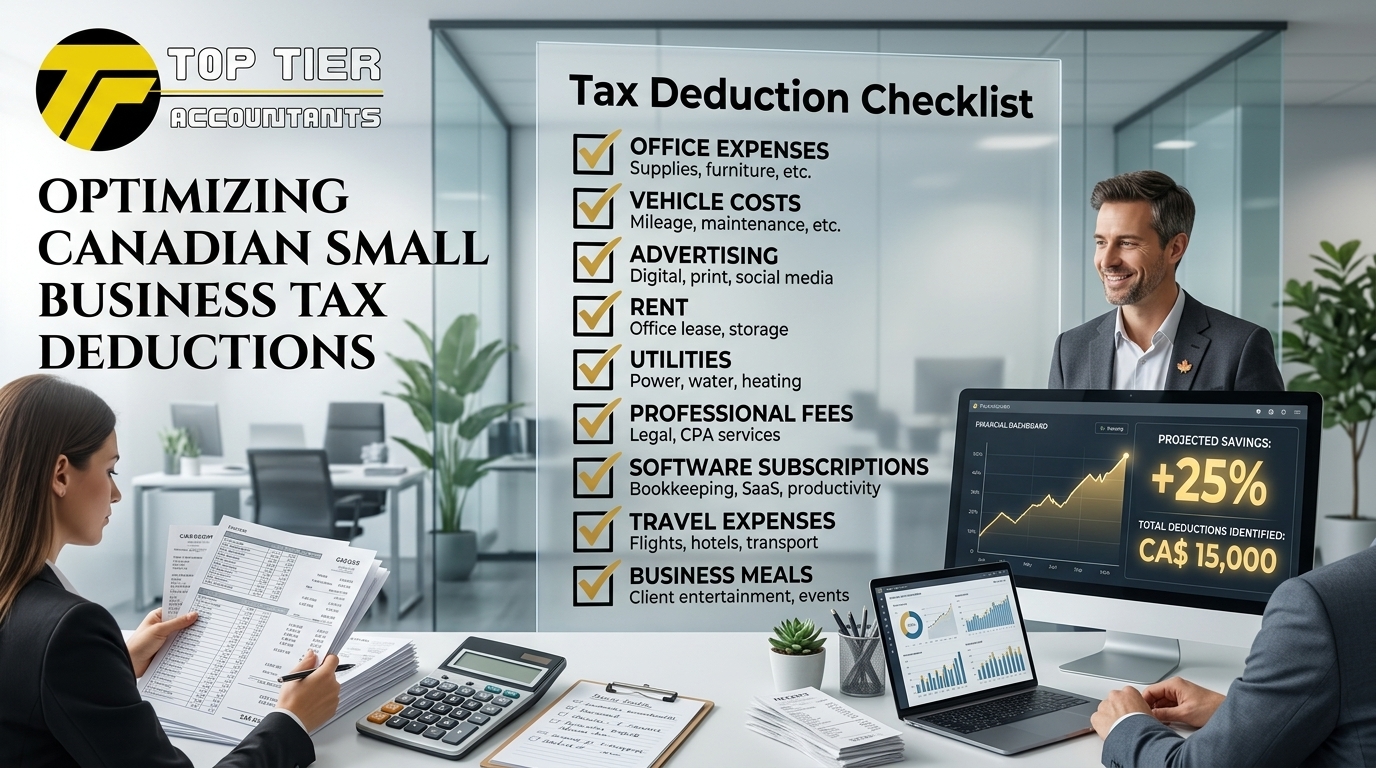

Maximizing Deductible Business Expenses

One of the simplest ways to reduce taxes is claiming every eligible deduction.

A business expense is deductible if it is reasonable and incurred to earn income.

Operating Expenses You Should Always Claim

Many businesses miss deductions simply because they forget to track them.

Common deductible expenses include:

- Advertising and marketing

- Office supplies

- Business insurance

- Accounting and legal fees

- Internet and phone services

- Rent and utilities

- Bank charges and loan interest

These costs directly reduce your taxable income.

Capital Cost Allowance and Asset Depreciation

Larger purchases such as equipment, computers, and vehicles must usually be claimed through Capital Cost Allowance (CCA).

Instead of deducting the full cost immediately, CCA spreads the deduction across several years.

Canada also allows accelerated depreciation incentives, enabling businesses to deduct more of an asset’s value in the first year of ownership.

This strategy helps businesses recover costs faster and improve short-term cash flow.

Salary vs Dividends Strategy

One of the biggest decisions for incorporated business owners is how to pay themselves.

Should you take salary, dividends, or both?

Benefits of Paying Yourself a Salary

Salary payments create RRSP contribution room and CPP benefits, which can be valuable for long-term retirement planning.

Salary also:

- Reduces corporate taxable income

- Provides predictable personal income

- Builds CPP pension eligibility

Advantages of Dividends for Tax Efficiency

Dividends don’t require CPP contributions, which can reduce payroll costs.

They also offer flexibility because owners can declare them when needed.

Many accountants recommend a balanced mix of salary and dividends to achieve optimal tax efficiency.

Income Splitting Strategies

Income splitting allows business owners to legally distribute income among family members in lower tax brackets.

Paying Family Members Legitimate Salaries

If family members genuinely work in the business, you can pay them reasonable wages.

This shifts income from higher tax brackets to lower ones, reducing the family’s overall tax burden.

However, salaries must reflect actual work performed to comply with tax rules.

Strategic Timing of Income and Expenses

Timing matters in tax planning.

Deferring Income to Lower-Tax Years

If your business expects lower income next year, deferring revenue can reduce taxes.

Similarly, accelerating expenses before year-end can reduce taxable income in the current year.

This strategy is especially useful during high-profit years.

Using Tax Credits and Incentives

Tax deductions reduce income, but tax credits reduce taxes directly, making them extremely valuable.

One of Canada’s most generous programs is the Scientific Research & Experimental Development (SR&ED) tax credit.

This program can provide up to 35% tax credits on eligible R&D expenses, dramatically reducing innovation costs.

Businesses investing in technology, software development, or product innovation often qualify.

GST/HST Planning for Small Businesses

GST/HST planning is another area where businesses can save money.

If your revenue exceeds $30,000 annually, you must register for GST/HST.

Once registered, businesses can claim Input Tax Credits (ITCs) on the GST/HST paid on business expenses.

These credits offset the tax you collect from customers, reducing the amount you must remit.

Proper GST/HST tracking can significantly improve cash flow.

Conclusion

Tax planning is not something to think about once a year—it’s an ongoing strategy that can dramatically impact your business profitability.

Canadian small businesses benefit from numerous tax advantages, including the Small Business Deduction, deductible expenses, income-splitting strategies, and tax credits. When used effectively, these tools can save thousands of dollars every year.

The key is proactive planning. Businesses that monitor expenses, structure income strategically, and leverage available incentives consistently outperform those that treat taxes as an afterthought.

Working with a knowledgeable accountant or tax advisor can help you identify opportunities that many entrepreneurs miss. With the right approach, you can reduce your tax bill, strengthen your financial position, and reinvest more profits into growing your business.

FAQs

1. What is the small business tax rate in Canada in 2026?

The federal small business tax rate is 9% on the first $500,000 of active business income, with additional provincial taxes bringing the combined rate to roughly 11%–13% in most provinces.

2. Is incorporation always better for tax savings?

Not always. Incorporation usually benefits businesses with consistent profits that can be reinvested rather than withdrawn immediately.

3. Can small businesses deduct home office expenses in Canada?

Yes. If your home is your primary place of business or used regularly for business activities, you can deduct a portion of utilities, rent, and other household expenses.

4. What is the biggest tax advantage for incorporated businesses?

The Small Business Deduction, which reduces the federal corporate tax rate from 15% to 9% on eligible income.

5. How can small businesses legally reduce taxes?

Common strategies include maximizing deductions, using salary/dividend planning, claiming tax credits, timing income and expenses, and choosing the right business structure.

Post a comment

Related Posts

June 5, 2026

What Expenses Are Tax Deductible for Small Businesses in Canada?

What Expenses Are Tax Deductible for Small Businesses in Canada? Running a small business in…

June 4, 2026

Common Bookkeeping Mistakes Small Businesses Make in Canada

Common Bookkeeping Mistakes Small Businesses Make in Canada Running a small business in Canada is…

June 4, 2026

Cash vs Accrual Accounting in Canada: Which Method Is Better for Your Business?

Cash vs Accrual Accounting in Canada: Which Method Is Better for Your Business? Running a…

May 18, 2026

How to Pay Yourself From a Corporation in Canada: Salary, Dividends, or Both?

How to Pay Yourself From a Corporation in Canada: Salary, Dividends, or Both? Running a…